5min

walk-up to boarding

Already enrolled at the bank. Walks up, scans, boards.

- Biometric already on file with the bank

- Scans palm vein at the airport gate

- Boards

Integrating biometric identity across two highly regulated industries, a first for Korea.

Two passengers, two paths

Same airport. The only thing that changes is whether their bank-side enrollment travels with them.

5min

walk-up to boarding

20min

queue, paperwork, re-enrollment

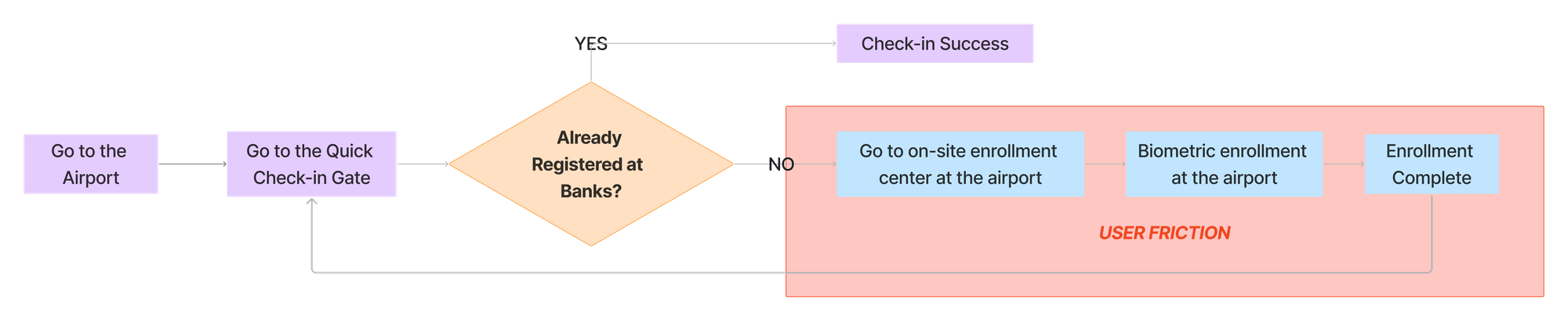

The bottleneck isn't the scanner. It's the re-registration. Korean users had to enroll their biometrics from scratch at every airport, even though their bank already had them on file.

TL;DR

Problem

Korean users had already enrolled their biometrics with their banks. Airports still forced a 20-minute re-registration. The reframe: make trust portable instead of rebuilding it.

Strategy

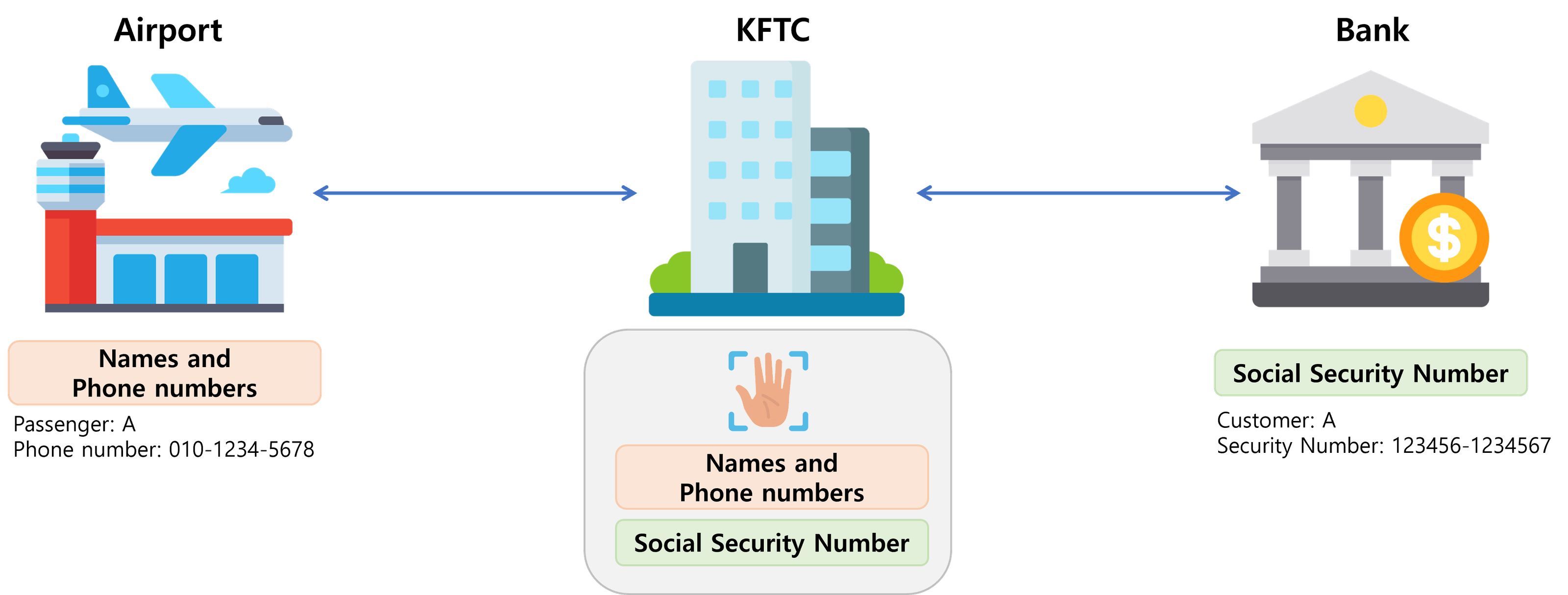

Instead of 168 direct bank↔airport integrations, I routed everything through KFTC, Korea's financial-clearing institution. I defined phone number as the primary identifier. This step bought regulatory approval and national reach.

Impact

First-ever nationwide cross-industry biometric framework. 500K users enabled within one year. 75% reduction in airport registration time. 12 banks · 14 airports.

Problem solved

The 20-minute re-registration looked like a UX problem. It wasn't. Two regulated industries can't legally share their default identifier, and they need a neutral third party between them.

The real challenge wasn't the queue. It was reusing trust across two regulated industries, without merging their identity systems or breaking privacy law. Banks used SSN. Airports were legally prohibited from using it. Mixing financial identity with travel data was unacceptable to regulators.

How I validated

I mapped stakeholders across banks and airports, and reviewed the relevant regulations on each side: banking, aviation, and PIPA. Together they surfaced the critical insight that reshaped every downstream decision:

Phone number was the only identifier held by both sides at non-sensitive level.

Why phone number? Already familiar to users. Less sensitive than SSN. Sufficient to map identities without reconstructing them. That reframed the work, from “build a new identity layer” to “bridge the one identifier they can share.”

Strategic pivot

Routing through KFTC turns 168 infrastructure integrations into 26, and a single trust contract both sides already accept.

rejected · direct

Each bank would need to integrate with each airport directly. Far too many integrations to maintain — wouldn't scale or last.

rejected · SSN

Banks already used it. Airports were legally prohibited from accepting it.

selected · KFTC + phone-number

KFTC bridges the connection; mapping data only. This step has reduced the service and regulation complexity into 5-month.

How I built · integration architecture

Routed all banks and airports through KFTC, while maintaining each governance and policy at maximum.

Financial identity never crossed to airports. KFTC stored only the phone-number mapping — never biometric data itself.

Bank enrollment did not silently extend to airport contexts. Users had to actively re-consent.

Phone-number changes get updated through bank channels, invalidate old mappings instantly, and require fresh consent when a number is reassigned to a new owner.

Before & after

Impact delivered

500,000 users

Enabled for biometric airport check-in within one year of launch

75 percent

Reduction in airport registration time

20 min → <5 min

5 months

Regulatory approval timeline

vs. 18+ months projected for direct integration

12 banks plus 14 airports

Banks + airports nationwide

defined the national interoperability standard

More on biometric systems

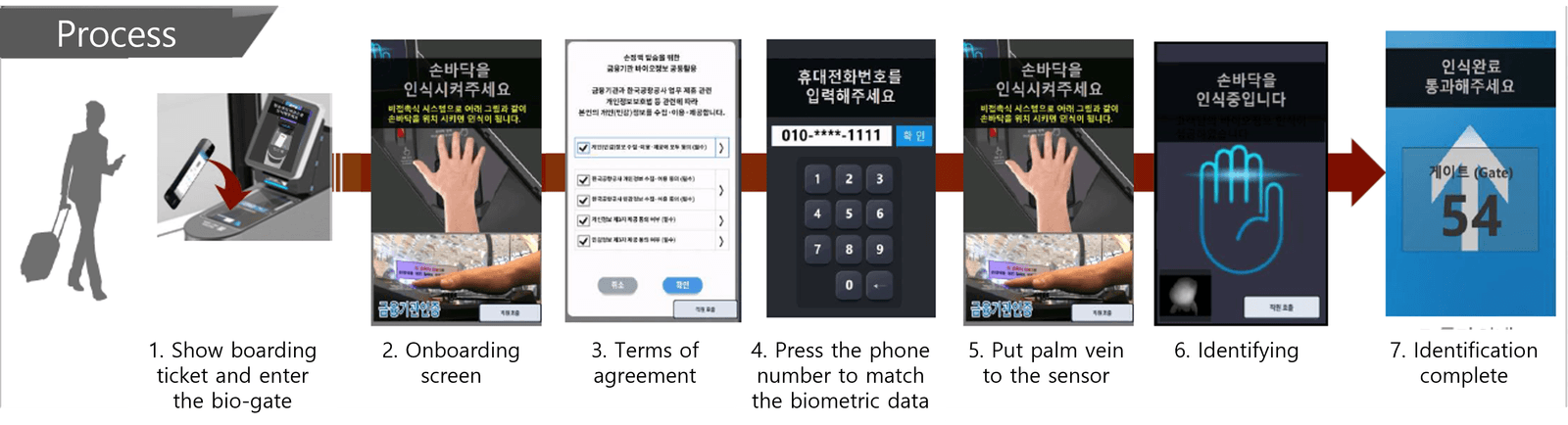

Banks and airports both used 'palm vein' for the main biometric data. Banks deployed the systems in the kiosks to identify the customer identity, whereas airports leveraged them at the check-in systems.

Key Takeaways

The highest-leverage product moves are often architectural: sit between parties who don't naturally trust one another, and give them a structure both sides can say yes to.